Making sense of the markets this week: January 21, 2024

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

Bitcoin goes mainstream—the exact stream that was supposed to run dry

I remember a few short years ago, bitcoin truthers were all about sticking it to the big financial companies and proving that they didn’t need traditional platforms.

“Keep your fiat currencies and your archaic trading systems!”

“Bitcoiners can buy and sell whenever they want, in whatever way the ‘revolutionary blockchain’ would allow.”

“All hail technological progress!”

That’s why I found it surprising how much hype there was last week for the big “Cointucky Derby” that saw 11 new bitcoin exchange-traded funds (ETFs) hit U.S. stock markets at the same time.

Suddenly, traditional financial stalwarts, like Fidelity and Blackrock, were not to be replaced and looked down upon as “yesterday’s money.” Oh, no, no, no. Now they’re going to be the salvation of the entire crypto asset class.

Gone are the days of “trade anywhere, anytime” and “not your keys, not your crypto.”

Instead, as a currency, bitcoin is embracing becoming just another ticker symbol going up and down on a stock exchange. Last year I interviewed PWL Capital’s Ben Felix at the Canadian Financial Summit. He explained how bitcoin has mastered the tactic of the constantly changing narrative.

First, it was going to be currency—until it wasn’t. Then it was going to be a diversifying asset, like gold—until it was highly correlated to tech stocks and other “risk-on assets.” Then it was going to be anti-inflationary—until it went down right as inflation skyrocketed.

So, now it’s going to be a great ETF ticker symbol to gamble on.

In case you missed the Cointucky Derby headlines, here’s a quick primer on where the world stands with regard to bitcoin ETFs.

- 11 bitcoin ETFs started trading in the U.S. last week.

- If you thought bitcoin ETFs existed before last week, you’d be correct. The U.S. actually had several derivative-based bitcoin ETFs, but the new ones more closely track the spot price of bitcoin.

- Wait, haven’t we actually had spot-price bitcoin ETFs for years? Well, yes, anyone in the world has been able to purchase a bitcoin ETF on the Toronto Stock Exchange since 2021. But everyone knows something doesn’t matter until it has made it in the U.S.

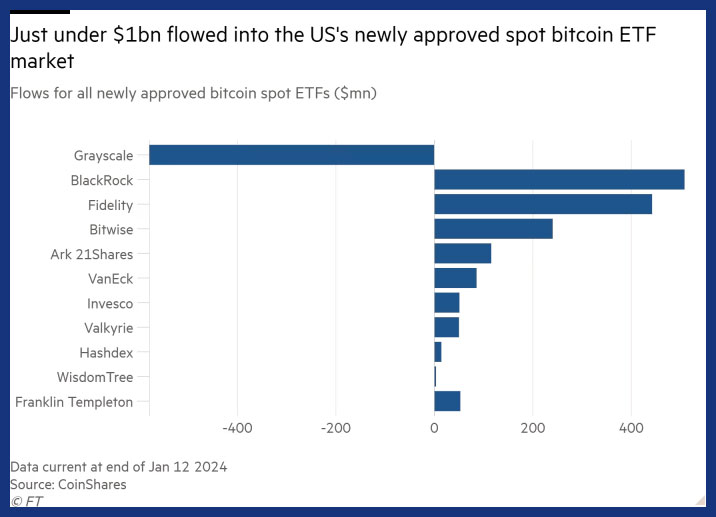

- The first three days of trading saw about USD$871 million of new flow into the collection of bitcoin ETFs.

- Most of the money that moved around within the bitcoin ETF space belonged to investors switching from the relatively high-fee Grayscale ETF (previously a derivative-based bitcoin ETF, but now a spot-price bitcoin ETF) to the newer, lower-fee options.

- The price of bitcoin has fallen about 6% since the new bitcoin ETFs started trading last week.

Yup, you read that last one correctly.

With a lot of speculative traders “selling the news,” the price of bitcoin has actually gone down since American traders were given access to bitcoin ETFs. It appears the massive run-up in bitcoin prices since October represented a “pricing in” of demand, boosted due to the new ETFs.

After all that pomp and circumstance, the grand predictions of a USD$100-billion inflow in the first year of bitcoin ETFs look quite silly. To put that USD$871-million figure in perspective, it’s much less than 1% of the total market capitalization of bitcoin. It’s also about 0.035% of the value of Microsoft.

The latest U.S. bank earnings reports

American banks had a fairly strong quarter and didn’t surprise much in either direction.

Bank earnings highlights

All earnings and revenue numbers below are reported in U.S. currency.

- JPMorgan (JPM/NYSE): Earnings per share of $3.04 (versus $3.32 predicted). Revenue of $39.94 billion (versus $39.78 billion estimated).

- Bank of America (BAC/NYSE): Earnings per share of $0.70 (versus $0.68 predicted). Revenue of $22.10 billion (versus $23.74 billion predicted).

- Wells Fargo (WFC/NYSE): Earnings per share of $1.29 (versus $1.17 predicted). Revenue of $20.48 billion (versus $20.30 billion predicted).

- Morgan Stanley (MS/NYSE): Earnings per share of $0.85 (versus $1.01 predicted). Revenue of $12.90 billion (versus $12.75 billion predicted).

- Citigroup (C/NYSE): Earnings per share of $0.84 (versus $0.81 predicted). Revenue of $17.44 billion (versus $18.74 billion predicted).

- Goldman Sachs (GS/NYSE): Earnings per share of $5.48 (versus $4.27 predicted). Revenue of $11.32 billion (versus $10.96 billion predicted).

JPMorgan had perhaps the most notable quarter, despite its headline earnings-per-share number dipping 15% from last year. Its CEO, Jamie Dimon, explained on a conference call that there was a $2.9-billion fee tied to the regional banking crisis and the acquisition of First Republic Bank. Consequently, the bottom line looks less healthy than the underlying business numbers would indicate.

The acquisition looks to be turning out quite well for America’s largest bank, as it claimed that the former First Republic Bank contributed $4.1 billion in profit in 2023.

Dimon provided some macroeconomic context in forward guidance. “The U.S. economy continues to be resilient, with consumers still spending, and markets currently expect a soft landing.”

Of course, being a banking CEO, he then had to hedge his position by saying deficit spending “may lead inflation to be stickier and rates to be higher than markets expect.”

New Morgan Stanley CEO Ted Pick cited two “major downside risks” as reasons for concern: geopolitical conflicts and the U.S. economy.

Mirroring Dimon’s “on one hand, and on the other hand” PR formula, Pick stated, “The base case is benign, namely that of a soft landing. But, if the economy weakens dramatically in the quarters to come and the [U.S. Federal Reserve] has to move rapidly to avoid a hard landing, that would likely result in lower asset prices and activity levels.”

Like their Canadian banking brethren, the U.S. banks all reported substantial increased provisions for credit losses. This money, set aside to cover the inevitable increase in interest-led loan delinquencies, also weighs on banks’ bottom lines.

Canadians looking for exposure to U.S. banks can get it through TSX-listed ETFs, such as the Harvest US Bank Leaders Income ETF (HUBL), RBC U.S. Banks Yield Index ETF (RUBY) and BMO Equal Weight US Banks Index ETF (ZBK). Investors can also get single-stock exposure to JPMorgan, Bank of America and Goldman Sachs in Canadian dollars through Canadian Depository Receipts (CDRs) listed on the Cboe Canada Exchange.

Check MoneySense’s ETF screener for all ETF options in Canada.

Interest rate: 2.50%. Get 0.50% additional bonus interest when you set up an eligible recurring direct deposit or preauthorized debit withdrawal of at least $500 each month.

$0 commission on all transactions. No minimum deposit needed.

If you’re looking to lock-in the highest GIC rates in Canada, view our list of Canada’s top GICs for 2024.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Delta benefits from revenge travel; attention, turbulence ahead

Delta (DAL/NYSE) was one of the first big travel companies to report December earnings results late last week. As the largest airline in the world, its insights on consumer travel patterns are always interesting.

Delta’s earnings highlights

All figures in U.S. dollars.

• Delta (DAL/NYSE): Earnings per share of $1.28 (versus $1.17 predicted). Revenue of $13.66 billion (versus $13.52 billion estimated).

It was an interesting earnings call for Delta. Obviously, anytime fourth-quarter profit doubles and beats estimates, it’s good news. However, the airline’s share price plunged 9% due to its CEO, Ed Bastian, announcing company forecasts of a gloomier 2024 than previously expected.

Delta shared the following travel insights:

- “Business is going great. Just go to any airport.”

- Currently there is a slight oversupply of seats for American domestic flights, resulting in better deals for off-peak fares.

- “Revenge travel has years to go, particularly in long-haul international. People in their retirement years want to travel. We weren’t able to accommodate them all last year.”

- “Early returns for spring and summer are very favourable. We had a fantastic year in the transatlantic. We are hoping to beat that.”

- The death of the business travel and premium travel classes has been greatly exaggerated. In the fourth quarter, record numbers of premium cabin seats were sold, and revenue was up 15% (compared to 10% revenue growth from standard coach seats).

If Canadian airlines are more your thing, you can check our piece on investing in Canadian airline stocks at MillionDollarJourney.com.

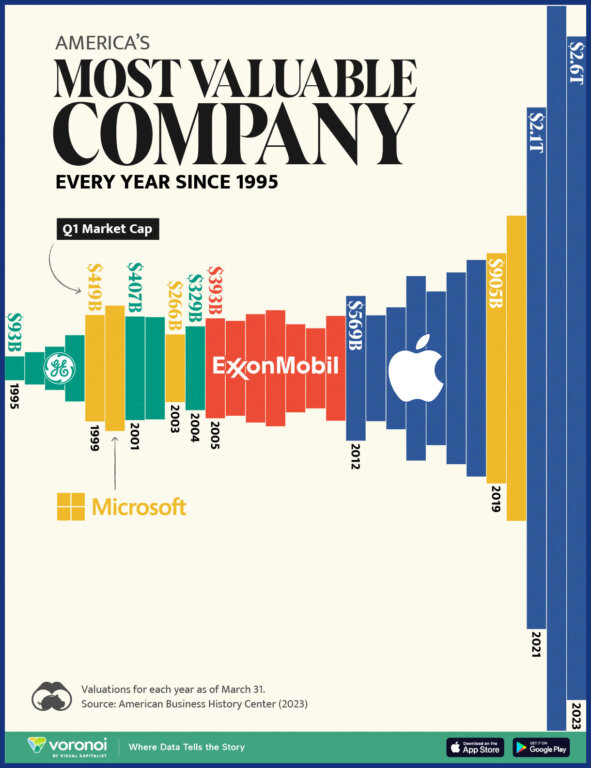

Microsoft is the new heavyweight champ of market cap

Microsoft (MSFT/NASDAQ) passed Apple (APPL/NASDAQ) last Friday in the never-ending race for market capitalization supremacy.

Most investors use the metric of market capitalization as the measurement of a company’s size. And that can lead most market watchers to state that Microsoft was reclaiming the title of world’s biggest company after several years of Apple sitting at the top. The small gap between the two companies (what’s a few billion between tech friends?) actually opened slightly wider this week.

Microsoft’s share price appreciation is mostly due to artificial intelligence (AI) buzz and the success of the company’s cloud computing unit. Neither of these is a major factor for the hardware and services success that Apple hangs its hat on.

The news wasn’t all bad for Apple, though, as it officially became the world’s biggest seller of smartphones this week, taking that title from Samsung, which carried it for over 12 years.

Here’s a look at who has held the market cap title over the past few decades. It’s interesting to note that General Electric has fallen all the way to 90th, just ahead of RBC, while Exxon Mobil is 19th.

Read more about investing:

- How might inflation impact your retirement plans?

- What is a cashable GIC?

- Will GIC rates keep going up in 2024?

The post Making sense of the markets this week: January 21, 2024 appeared first on MoneySense.

No comments