What does opening or cancelling a credit card do to my credit score?

Ask MoneySense

Now seems to be a good time to take advantage of a welcome offer on a new credit card. What does it do to my credit score when I open and close credit cards?

—Charlie

How changing credit cards affects your credit history

Thank you for the question, Charlie. It’s important to be thoughtful about how your use of a credit card impacts your credit score, which is an indicator of creditworthiness for lenders. We’ll walk you through the impact of opening and closing credit cards on your credit score and offer some tips on how to minimize damage. Over and above what happens to your credit score, it is also important to understand how these actions will affect your ability to live within your means and manage your debt.

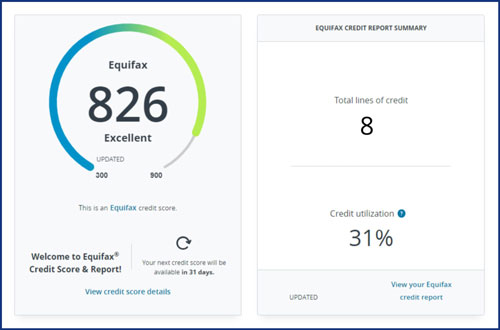

How are credit scores calculated?

Your credit score is calculated by credit bureaus that convert information on your credit report to a number based on a formula called the FICO formula. Your credit score will be a number between 300 and 900. You can obtain your credit score for free through one of Canada’s two credit bureaus, Equifax or TransUnion. Also, most major Canadian banks allow you to access your credit score free online through their online banking platforms.

What is a credit score?

Below are the factors that make up your credit score. Each is assigned a percentage indicating how important they are when it comes to calculating your score:

| Factor | What that means to you | Weighting in credit score | What you can do |

| Payment history | How timely you are with payments on past and current debt. Missed payments or payments that are less than the minimum amount may drop your score. | 35% | If you can’t pay your balance off in full each month, make at least the minimum payment on time to avoid a negative impact on your credit score. |

| Credit utilization | How much credit you are using, and how likely you are to be able to pay any debts back. | 30% | Keep the amount of credit you use to under 30% of what’s available to you. For example, if you have $10,000 in total credit available, use no more than $3,000 at any given time. |

| Credit history | The length of time you have been using credit. It helps predict credit use behaviour. | 15% | Keep your oldest credit card open, even if you don’t use it regularly. |

| Diversity of credit | The different types of credit you have, from the number of credit cards to loans and lines of credit. It shows your ability to manage multiple payments. | 10% | If you only have one credit card reporting to the credit bureaus, and if the issuer offers a line of credit, accept it—but use it sparingly or not at all. |

| Hard credit inquiries | The number of times you apply for new credit. Not all inquiries are hard or impact your score—a soft inquiry is when your credit score is checked for another purpose, say for a job application or just because you’re curious. | 10% | Only apply for new credit products that you need, and only apply for one at a time. |

How opening and closing credit cards can affect your credit score

Your credit score can impact what loans you qualify for, the interest rate you’ll pay, what you can afford, where you work, and where you live. So, it is important to understand how your credit score is calculated and what actions may impact it. Now that you understand the calculation, here’s how it may affect the above weighting in your overall score.

Payment history: Opening and closing credit cards doesn’t directly affect payment history unless having more access to credit makes it harder for you to pay your bills.

Credit utilization: If your credit card is maxed out, trying to open a new card might bring down your score, as it could be seen as a warning sign to new creditors that you are having problems paying down your existing balances.

Credit history: The older credit card would be considered more reliable to use in predicting behaviour than a brand new file that was recently opened. So keep a long-standing credit card in your wallet that you never close, even if you have another that has a better interest rate or rewards.

Diversity of credit: Lenders and creditors like to see that you have a diverse credit mix, such as mortgages, loans and credit cards. However, it will only positively impact your score if you’ve been able to manage these different types of credit accounts responsibly over time.

Hard credit inquiries: When you apply for a new credit card, the credit company will perform a hard pull of your credit report for review as part of the approval process. This hard inquiry on your credit history will lower your score; however, the impact is generally low on the FICO scale.

Earn 5 times the points on groceries and restaurants. Redeem points for flights on any airline.

An ideal option for cardholders looking to manage debt, the card’s low 12.99% APR is almost half the conventional interest rate found on most cards.

Earn 4% cash back on groceries, plus 4% on recurring bills and 2% on transit.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

What happens when you apply for a new credit card

When you apply for a new credit card on top of one you already have, lenders will perform a hard inquiry on your credit history to help determine whether you’re a good candidate for their product.

Any time your credit experiences a hard inquiry, it will drop a few points. If it’s only one inquiry (meaning one credit card and not multiple cards from different providers), then the negative impact to your score will be minimal.

However, if suddenly there are a large number of hard inquiries to your report, your score will take a hit and creditors will question why you are applying to so many lenders at once.

On a positive note, opening a new credit card gives you an opportunity to reduce your credit utilization ratio since your total available credit is being increased.

For example: If you have one credit card with a balance of $7,000 and a limit of $10,000, your credit utilization is 70%. If you add a new card with a $10,000 limit and your balance remains $7,000, the total limit of your two credit cards is $20,000, bringing your credit utilization down to 35%.

And that’s good, remember, from the chart above.

However, lenders want to see you using your credit in a responsible way. If you open multiple new cards to try to reduce your credit utilization ratio but don’t make improvements to your payment history, this will have a negative impact on your score.

What happens when you cancel a credit card

When it comes to cancelling a credit card, simply closing the account isn’t a problem. But it will increase your credit utilization ratio.

To close a credit card, the balance is $0. If there’s a substantial balance on the remaining cards, it’s going to increase the credit utilization ratio. And, if the increase is high enough, it will hurt your credit score. This is because the closed card’s unused credit limit no longer provides balance in the relationship between your other credit balances and credit limits. What you owe elsewhere can have a bigger impact than if you had a zero-balance credit card.

Another thing: Closing an account means the creditor will stop reporting on your behalf your credit history on that card. If the card showed positive credit history, such as responsible usage and making payments on time, that history will gradually fade away and no longer bolster your credit score.

The reverse can’t be said. If the card showed negative credit history, closing the account will not erase the negative impact on your score.

Generally speaking, cancelling a credit card won’t improve your credit score, and you shouldn’t close a credit card unless you have a good reason, such as not trusting yourself to use the credit responsibly.

Buyer beware: Welcome offers

Many credit cards come with a generous sign-up bonus that helps you earn cash back, points, miles or a reduced interest rate. Welcome offers can be a great way to save money, especially if you already had planned on spending the minimum threshold to earn them. However, proceed with caution.

Read the fine print. Despite the enticing welcome offer of a credit card, your credit score may drop when you apply for a new card as a hard inquiry will be performed during the application process. Although your credit score will only drop a couple of points and will likely recover after a few months if you make your payments on time, it’s still a hit to your credit.

Remember that welcome offers are one-time deals. While some credit card sign-up bonuses may save you money up front, the reality is that any rewards you earn aren’t worth incurring additional bills if you’re already struggling with debt. You should only consider a new welcome offer if you have paid off your credit card debt in full. If you have any debt, focus on paying that down—not short-term wins like getting a lower and very temporary interest rate.

Opening and closing credit cards can impact how you use credit, too. Open multiple new cards, and you may end up with more credit than you can feasibly handle or keep track of. In addition, the allure of welcome offers may distract you from your financial goals. There’s impact on your credit score, and it’s critical to think about how having more or less credit affects your ability to live within your means and pay off your debt in full each month.

Should you swap credit cards?

While welcome offers can make signing up for new credit cards enticing and increase the amount of credit available to you, only apply for a new card if you can pay the bill in full each month. The application process and any missed payments can negatively impact your credit score and your financial goals.

Charlie, understanding how opening and closing credit cards can impact your credit score may seem intimidating. However, once you know how your score is calculated and what information is utilized, you can make informed decisions that will help you reach your financial goals.

As a professionally certified credit counsellor with Credit Canada, we can help you understand your credit score and how certain decisions impact it. If you need additional support, contact Credit Canada today to book a free credit-building counselling session.

This article was created by a MoneySense content partner.

This is an unpaid article that contains useful and relevant information. It was written by a content partner based on its expertise and edited by MoneySense.

Read more about credit score and credit history:

- Credit card mistakes and the secret to avoiding the impulse buy

- Good habits that can help you improve your credit score

- 6 things you didn’t know could be hurting your credit rating

The post What does opening or cancelling a credit card do to my credit score? appeared first on MoneySense.

No comments