Making sense of the markets this week: February 11, 2024

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

Disney is back on track

Even with all the iconic brands under its corporate umbrella, Disney has struggled the last few years, as its share price is down 11% since February 2019.

Things might be looking up now that CEO-extraordinaire Bob Iger is back in the captain’s seat after “retiring” back in 2020.

Disney earnings highlights

All earnings and revenues for Disney, PayPal, McDonalds, and Eli Lilly below are in U.S. dollars.

• Disney (DIS/NYSE): Earnings per share of $1.22 (versus $0.99 predicted), and revenues of $23.55 billion (versus $23.64 billion predicted).

Disney shares were up over 7% in extended trading on Wednesday after the earnings call. And the call highlighted the following reasons for increased profit guidance in 2024:

- Disney will meet or surpass its goal of cutting costs by $7.5 billion this year.

- The House of Mouse company will also invest $1.5 billion into a partnership with game software developer Epic Games.

- Disney’s “experiences” division (think theme parks and cruises) saw a 7% increase in revenues versus last year.

Yet, the biggest Disney revelation this week came from its sports streaming division.

With Amazon trying live football broadcasts this year, it appears the more traditional names in media have decided to fight back.

Disney (through its ESPN subsidiary), Fox and Warner Bros. Discovery announced joining forces to create a new sports streaming service. The planned platform has yet to be named, but it would feature current sports programming from ESPN, ESPN2, ESPNU, SECN, ACCN, ESPNEWS, TNT, TBS, TruTV, FS1, FS2, BTN, UFC, as well as the main ABC and Fox broadcasts.

Iger stated, “The launch of this new streaming sports service is a significant moment for Disney and ESPN, a major win for sports fans and an important step forward for the media business.”

When you think about the possibilities of bundling a new live sports service with current Disney+, Hulu, and Max (the HBO streamer), you will have re-created a substantial amount of the old American cable bundle, plus streaming of classic movies and TV shows. Now, all we need to know is the price, and if and when it would be made available to Canadians.

Big Mac vs. big pharma

It was a lopsided earnings battle this week in the fight between fast food and appetite-suppressing drugs. Eli Lilly’s new drugs Mounjaro and Zepbound (its answer to Wegovy and Ozempic) continue to drive earnings and revenues growth.

Food and pharma earnings highlights

All figures here are in U.S. dollars.

Eli Lilly reported its sales of Mounjaro went through the roof ($2.21 billion in sales for the fourth quarter of 2023, up from $279.2 million during 2022’s fourth quarter). And it announced that its even newer weight-loss drug, Zepbound, is selling as fast as it can be manufactured.

Zepbound won Food and Drug Administration (FDA) approval in November 2023 and managed to ring up $175.8 million in sales during the last few weeks of 2023. Some experts believe Zepbound could eventually become the biggest selling drug of all time. Consequently, shares of Eli Lilly are up by about 60% over the last year.

Alas, it wasn’t slimmer waistlines worrying McDonald’s shareholders this week. It was the Muslim anti-American boycotts around the world. McDonald’s CEO Chris Kempczinski stated, “The company is monitoring the evolving situation, which it expects to continue to have a negative impact on systemwide sales and revenue as long as the war continues.”

Shares were down 4% on Monday after earnings were announced.

Long-term, it will be interesting to see if these weight-loss drugs reach enough people that it has a measurable effect on snack and fast-food companies. The more demand there is for Ozempic, Wegovy, Mounjaro, Zepbound and the successive generations of tirzepatide (the generic name for this drug), the more nervous I would get as a shareholder of companies that rely on our super-sized appetites.

Earn between 2.5% and 4% interest on your savings. Plus, use the pre-paid card for everyday purchases and free ATM withdrawls.

$0 commission on all transactions. No minimum deposit needed.

Interest rate: 5.40%

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

PayPal cuts 2,500 jobs, and still can’t save its share price

If you needed a reminder that headlines about “The Magnificent 7” don’t represent all tech stocks, PayPal gave a stark nudge this week.

PayPal earnings highlights

Figures are in U.S. dollars.

- PayPal (PYPL/NASDAQ): Earnings per share of $1.48 (versus $1.36 predicted) and revenues of $8.03 billion (versus $7.87 billion predicted).

Despite the earnings beat, shares were down 8% in extended trading on Wednesday. That drop means share prices are now down 28% over the last 12 months. And they’re down even more than 80% from their all-time high in July 2021.

My takeaways from the PayPal earnings call were:

- Revenue was up 9% for the quarter in a year-over-year (YOY) comparison.

- Net income was up 51% YOY.

- Active accounts were down 2%.

- PayPal will be cutting 9% of its global workforce (2,500 jobs).

- Earnings guidance for late 2024 was shifted downward.

Newly instated PayPal CEO Alex Chriss said, “We’re driving significant transformation across our company and are committed to making the necessary changes to our business to drive profitable growth in the years ahead.”

For me, that’s business-speak for: “Look, we’re still a good company, but we’re out of new ideas. We’re going to furlough a bunch of staff. And if that doesn’t work, we’ll still be here when the next pandemic comes around.”

Bell’s dividend is up—employee count is down

Usually, earnings calls for Canada’s major telecommunications are quiet affairs. Nothing-to-see-here types of events: Business as usual, profits slightly up.

That wasn’t the case this week.

Bell earnings highlights

The Canadian telcom released:

- Bell (BCE/TSX): Earnings per share of $0.73 (versus $0.76 predicted) and revenues of $6.47billion (versus $6.47 billion predicted). Share price was down 3.75% on Thursday.

While Bell’s earnings numbers were pretty close to its predicted targets and it was able to raise its annual dividend payment by 3%, it was its commitment to cost cutting over the next couple of years that attracted the most headlines.

Bell’s cost-cutting announcement included:

- Cut 4,800 jobs (9% of all BCE employees), on top of the 1,300 jobs lost in June

- 45 of its 103 regional radio stations will be sold off

- The staff reductions are expected to save the company about $250 million per year.

Bell wasn’t done with big announcements though, as it explained they would be massively paring back their capital expenditure plans by $1 billion.

In short, Bell chief legal and regulatory officer Robert Malcolmson explained in an interview that the company was done building fibre networks for its competitors to use. Previous plans included expansion of the fibre optic network to 9 million homes by the end of 2025. That plan has been reduced to 8.3 million.

This decision is in response to the CRTC’s announcement last November, that it was going to force Telus and Bell to allow smaller competitors to access the fibre networks in order to promote internet service competition.

“We can’t justify investing that capital when we’re just building a network for our competitors to resell,” Malcolmson said.

Bell representatives went on to explain that they were depending on the federal government to support Canadian media, and to delay the fibre regulatory changes, or inevitably more attempts at cost-cutting would be on the way.

You can see my take on Bell and other Canadian telecommunications stocks at MillionDollarJounrney.ca.

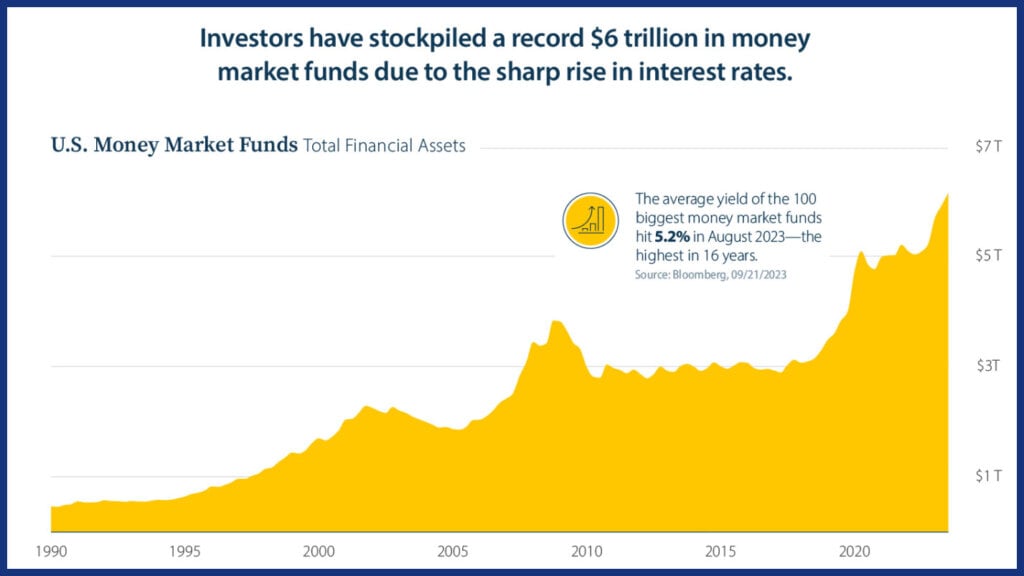

Put me in coach—I’m ready to buy

An interesting development that has bullish stock market watchers salivating: How much cash has piled up “on the sidelines” over the last couple of years. If you’re not familiar with this expression, it refers to investors holding back a lot of money from long term investments. It’s similar to the phrase “keeping your powder dry.”

This communicates how much money investors have socked away in their basic chequing accounts, high-interest savings accounts, short term bonds, guaranteed investment certificates (GICs) and money market funds. This graph and accompanying data from Visual Capitalist caught my eye, and it should catch yours too.

Source: Visual Capitalist

That’s American data, of course, but it appears the trend holds true here in Canada, as well. Canadians have built up “excess savings” of close to $400 billion.

I would hazard a guess that a solid chunk of that money is waiting for stock market risks to go away. It’s interesting to think about what will happen when even risk-averse investors finally feel secure enough to go back into more risky assets such as stocks again.

The S&P 500 has a total market cap of about USD$41 trillion. The entire Toronto Stock Exchange is worth about USD$2.6 trillion. Consequently, that “dry powder” (a.k.a. the cash “on the sidelines”) could make a pretty big impact if it explodes within the next couple of years.

Given all of the negative economic news headlines of the last few years, I don’t think all these overly cautious money-holders are going to rush back into the markets any time soon. But if interest rates start to gradually wind down, and the stock market continues to hit new all-time highs, then some of that cash is going to flow into riskier assets.

For more information on where to park cash while waiting for an investment opportunity, check out my article on the best low risk investments in Canada on MillionDollarJourney.ca.

Read more about investing:

- How might inflation impact your retirement plans?

- What is a cashable GIC?

- Will GIC rates keep going up in 2024?

The post Making sense of the markets this week: February 11, 2024 appeared first on MoneySense.

No comments