Making sense of the markets this week: March 31, 2024

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

You can’t handle the truth—Truth Social!

You might’ve read a headline like this the past week, “Trump’s social media company to trade on the Nasdaq.” While some might think there’s money to be made, the underlying transaction is substantially more complicated. If you’re looking for the Coles Notes version, know that this story is interesting in the same way as watching a fender bender on the highway holds everyone’s attention. No serious Canadian investor would consider going near this company. (All figures in this section are in US currency.)

Here’s how former president Donald J. Trump just might get paid from Truth Social (along with some caveats investors should know about):

- Truth Social was the only asset of record owned by a company called Trump Media & Technology.

- Truth Social has accrued a whopping total of $3.4 million in revenue over the last nine months, yet it’s still on its way to losing $49 million.

- Digital World Acquisition (DWAC) is a SPAC created in 2021, and its goal from day one was to raise enough money to eventually buy Truth Social. You might remember Special Purpose Acquisition Companies—better known as SPACs. I wrote about how useless SPACs tend to be about two years ago.

- DWAC has been trading on opening markets for several years now, with no actual underlying operating business. Essentially, it’s just a vague blank cheque for an eventual purchase of Truth Social. It inspired quotes like “DWAC is not just another dubious 2021 SPAC,” and “It’s a poster child for some of the worst abuses the investment vehicle has spawned.”

- DWAC was approved by the Securities and Exchange Commission (SEC) to purchase Truth Social for about $5 billion.

- After DWAC merged with Trump Media, the new company is called Trump Media and, as of Tuesday, trades under the ticker symbol DJT.

- On paper, Trump’s shares of Trump Media (which he received when DWAC merged with Trump Media & Technology earlier this month) were worth about $3 billion.

- After the first day of DJT trading on Tuesday, shares started at $38.00, briefly rose as high as $79.38, and then trended downward near the close of the day to finish at $57.99.

- As of the end of the day Tuesday, Trump’s stake in DJT was worth about $4.5 billion, before increasing another 17% Wednesday. It last traded at $67.69, for a market cap of $9.1 billion, lifting Trump’s personal stake to more than $5 billion.

- The catch here is, as the rules currently stand, that Trump and other shareholders cannot sell their shares for six months after the shares go public. This is a common rule (often referred to as a “lock-up period”) and is generally used to assure investors of no fraudulent activity.

- Of course, (who would’ve guessed?), Trump’s team is currently exploring options that would enable a board of directors to allow Trump to sell his shares before the lock-up period ends.

- If he doesn’t get approval to sell his shares before the lock-up ends, Trump will have to wait six months to sell. Only time will tell if investors will want to own expensive shares of a company that looks to have very little hope of making any money. If they do not, the share price in six months could be valued next to nothing.

From what I can tell, this whole transaction appears to be some odd combination of die-hard Trump fans wanting to support him financially, alongside get-rich-quick speculators looking to make a quick buck off of said fans. The share price in six months will depend on how many shares are held by each of the groups, as well as which foreign investors purchase shares with the intent of influencing a possible future president.

It should also be noted that both sides of the deal feature corporations that are currently embroiled in overlapping legal issues.

That doesn’t exactly sound like a long-term winner to me, but apparently billions of dollars of speculative “meme stock” cash would disagree with my analysis.

How is the original “get rich quick” meme stock doing?

Speaking of stocks that go way up for reasons outside of their financials and then leave investors holding billions of dollars worth of nothingness, let’s check in on the original meme stock: GameStop.

GameStop earnings highlights

All figures are in US currency.

- GameStop (GME: NYSE): Shares plunged 17% in after-hours trading on Tuesday, as earnings per share came in at $0.22 (versus USD$0.30 predicted), and total revenues of $1.79 billion (versus $2.05 billion predicted).

Here’s what the share price journey for GameStop has looked like over the last few years (and that’s before earnings were posted on Tuesday).

The shift from cartridge games to online games is an obvious blow to bricks-and-mortar retailers like GameStop. While GameStop may struggle on in some capacity for many years to come, it turns out that buying shares in a company that doesn’t make money is a bad long-term investment.

Anyone in DJT Land listening?

Drill baby, drill—but only in the USA, please

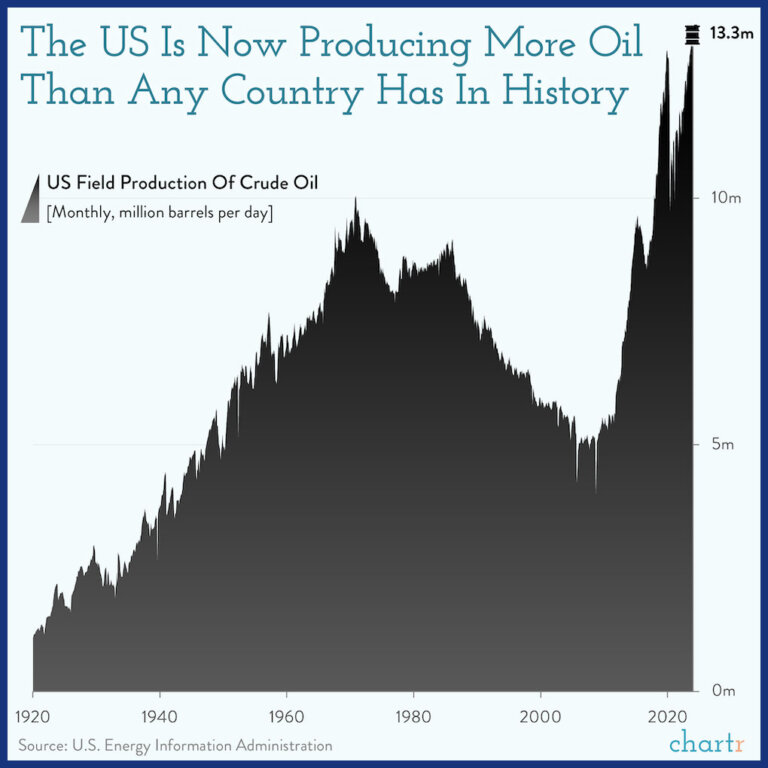

With so much going on in the world, it might have slipped past some Canadian investors that the US fossil fuel industry just hit an interesting milestone. America now has the honour of producing more oil in a single day than any other country in the history of our planet. Yes, even more than Saudi Arabia.

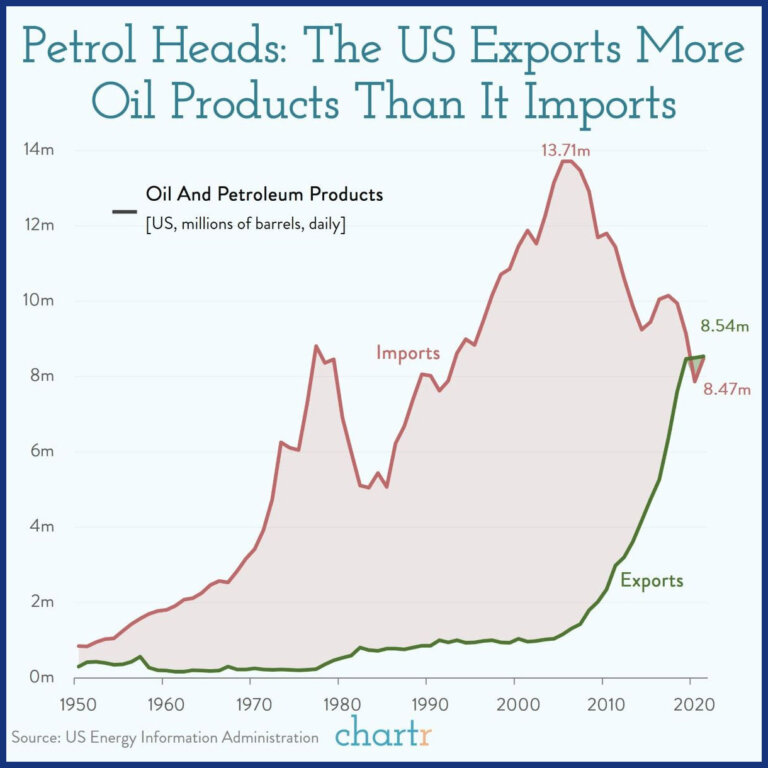

When you consider that the USA has been a massive oil importer for much of the last 70 years, it’s pretty noteworthy that the US exported four million barrels of oil per day last year.

It certainly appears that investors are not shying away from providing capital to American fossil fuel companies. It also means that Canadian efforts to turn away from natural gas (despite our allies essentially begging us for more yet again this week) may not add up to much in the great push against global warming.

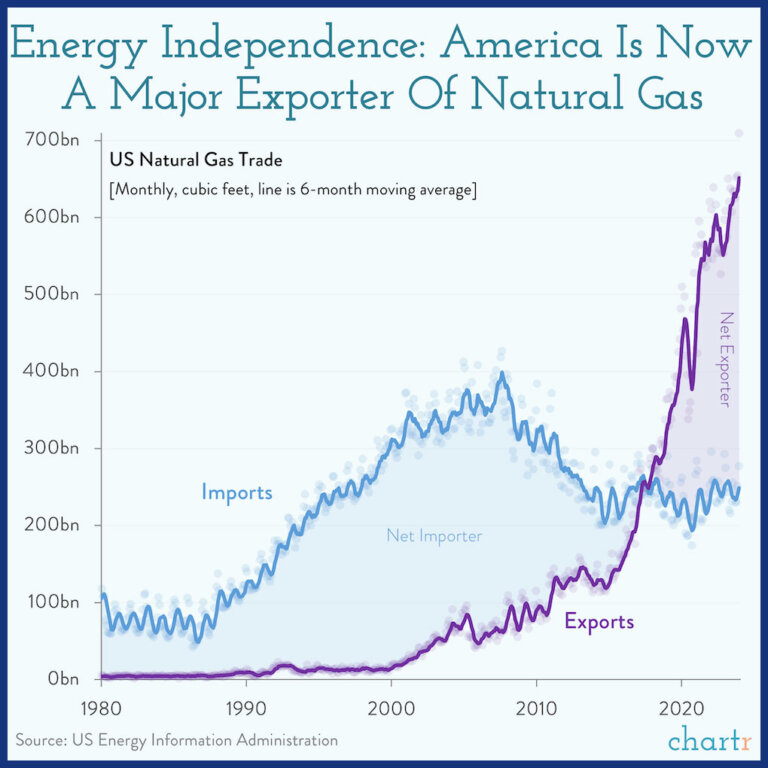

The USA is now the world’s largest exporter of natural gas, as well.

Wow, it’s a good thing the Keystone XL pipeline got cancelled, as it appears to have put a stop to all that American fossil fuel business—and at hardly any cost to the Canadian economy either!

Economists would argue that the best way, by far, to reduce the amount of fossil fuel being burned would be to put a tax on it. How popular is that tax on carbon these days anyway?

Clearly, the world has to decide on what sort of level playing field it wants to create in regards to the rules for carbon reduction efforts, as Canada’s attempt to go it alone doesn’t seem to be gaining much traction.

For more information check out my article looking at Canadian energy stocks in 2024 on MillionDollarJourney.ca.

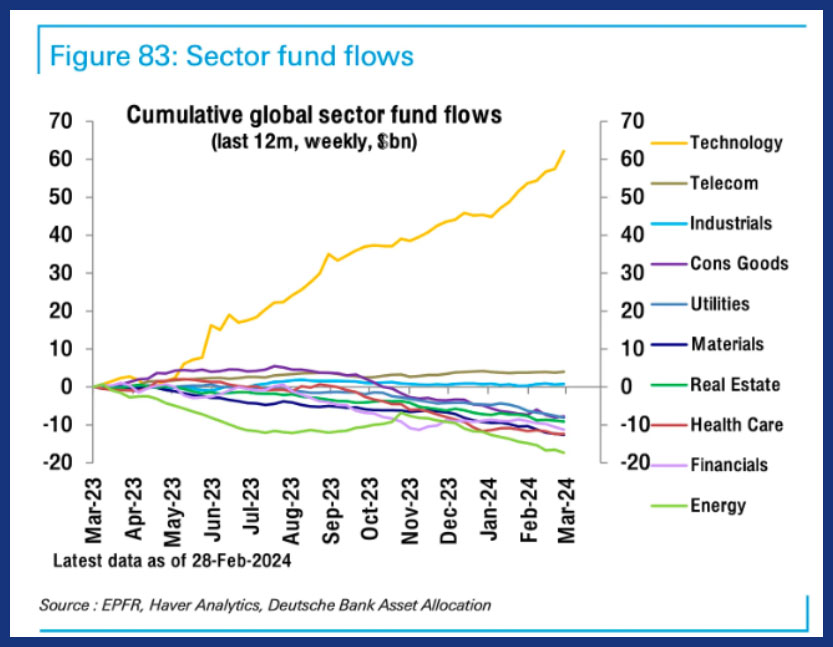

Tech versus everything else

Just in case it’s not crystal clear, the tech stocks in the S&P 500 have been growing at a rate that dwarfs everything else the past year.

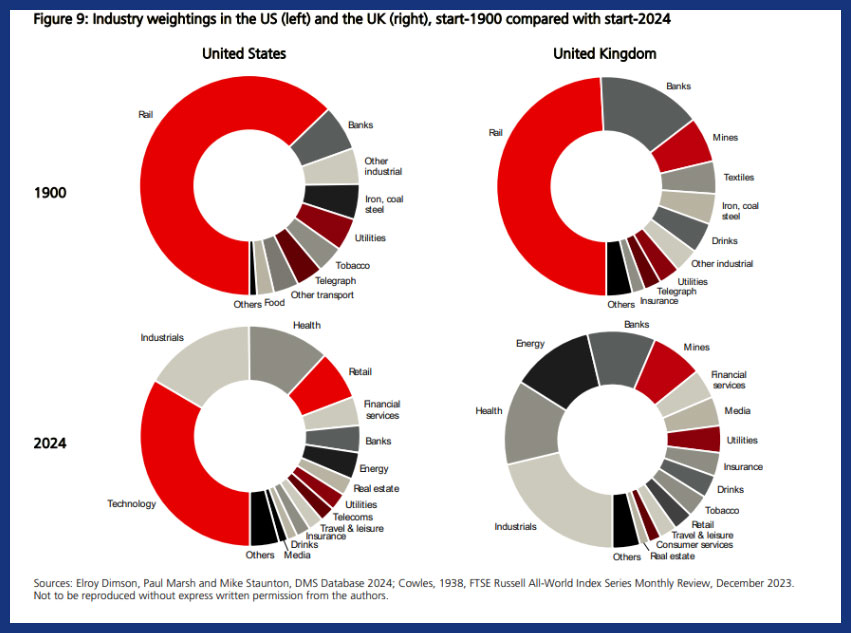

It’s interesting to note, though, that having the stock market being dominated by a specific industry is not necessarily new. Both the UK’s and the USA’s stock markets were much more railway-dependent in 1900 than the USA is on tech today—even after the recent run-up.

We look at it as a net positive that tech is dragging the rest of the S&P 500 along in the early stages of what could be quite a long bull market. In a perfect scenario, tech stocks will cool down and, as they pause for a year—or five—in order to grow into their valuations, other sectors of the market could take the baton and run with it. In this Goldilocks scenario, we could see various sectors move in and out of favour over the short term, but overall, markets would consistently trend upwards.

If we could use the exchange-traded fund (ETF) VCN as a proxy for Canada’s stock market, then it could be said that the Canadian P/E ratio is still at a very reasonable 16.8x. We also see that while it isn’t as diversified as the USA’s stock market, it’s not even close to as reliant on one industry as the USA was back in 1900.

One can always look at the pessimistic side of things and say things like, “An overvalued tech sector is the only thing driving the stock market.” But the flip side could be, “Tech is the only thing that has popped so far—just wait until some of the other sectors catch up.”

I’m not saying that plodding sectors like utilities and/or banks are going to go gangbusters like Nvidia. But I think it’s quite possible that even if tech falls back to Earth a bit, we could continue to see positive overall momentum for a long time yet.

Read more about investing:

- How might inflation impact your retirement plans?

- What is a cashable GIC?

- Will GIC rates keep going up in 2024?

The post Making sense of the markets this week: March 31, 2024 appeared first on MoneySense.

No comments